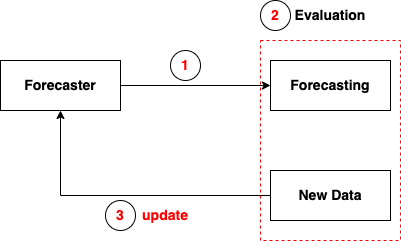

Model Creation¶

import warnings

warnings.filterwarnings('ignore')

from sktime.datasets import load_longley

_, y = load_longley() # 16*5

y.head()

| GNPDEFL | GNP | UNEMP | ARMED | POP | |

|---|---|---|---|---|---|

| Period | |||||

| 1947 | 83.0 | 234289.0 | 2356.0 | 1590.0 | 107608.0 |

| 1948 | 88.5 | 259426.0 | 2325.0 | 1456.0 | 108632.0 |

| 1949 | 88.2 | 258054.0 | 3682.0 | 1616.0 | 109773.0 |

| 1950 | 89.5 | 284599.0 | 3351.0 | 1650.0 | 110929.0 |

| 1951 | 96.2 | 328975.0 | 2099.0 | 3099.0 | 112075.0 |

from sktime.forecasting.model_selection import temporal_train_test_split

y_train, y_test = temporal_train_test_split(y, test_size=4) # hold out last 4 years

from sktime.transformations.series.detrend import Deseasonalizer

from sktime.transformations.series.func_transform import FunctionTransformer

from sktime.forecasting.trend import PolynomialTrendForecaster

from sktime.transformations.series.detrend import Detrender

def forward_transform(y):

return y*10

def backward_transform(y):

return y/10

trend = PolynomialTrendForecaster(degree=1)

# preprocessing pipeline

preprocessing = Detrender(forecaster=trend) \

* FunctionTransformer(func = forward_transform, inverse_func = backward_transform)

# preprocess training data

y_train_preprocessing = preprocessing.fit_transform(y_train)

import pandas as pd

def get_evaluation(df, name = 'test_MeanAbsoluteError'):

"""Extract evaluation information from cross-validation results

"""

evaluation = pd.DataFrame(columns = list(y.columns))

for trial in range(df.shape[0]):

row = {}

for index, feature in enumerate(list(y.columns)):

row[feature] = df[name][trial][index]

evaluation = evaluation.append(row, ignore_index = True)

return evaluation

# select model with a loop

import numpy as np

from sktime.forecasting.ets import AutoETS

from sktime.forecasting.var import VAR

from sktime.forecasting.varmax import VARMAX

from sktime.forecasting.model_evaluation import evaluate

from sktime.forecasting.model_selection import ExpandingWindowSplitter

from sktime.performance_metrics.forecasting import MeanAbsoluteScaledError

models = {'VAR': VAR(),

'AutoETS': AutoETS()}

fh=np.arange(1, 4)

cv = ExpandingWindowSplitter(step_length=4, fh=fh, initial_window=6)

loss = MeanAbsoluteScaledError(multioutput = 'raw_values')

for model in models:

df = evaluate(forecaster=models[model], y=y, cv=cv, strategy="refit", scoring = loss, return_data=True)

evaluation = get_evaluation(df, name = 'test_MeanAbsoluteScaledError')

print(model, ': ', evaluation.mean().mean())

VAR : 1.3518417095558566 AutoETS : 302.51897414372365

# select model with MultiplexForecaster

from sktime.forecasting.compose import MultiplexForecaster

from sktime.forecasting.model_selection import ForecastingGridSearchCV

models = MultiplexForecaster(

forecasters=[

('VAR', VAR()),

('AutoETS', AutoETS(auto=True, sp=12, n_jobs=-1))

])

fh=np.arange(1, 4)

cv = ExpandingWindowSplitter(step_length=4, fh=fh, initial_window=6)

forecaster_param_grid = {"selected_forecaster": ['VAR', 'AutoETS']}

model_selection = ForecastingGridSearchCV(models, cv=cv, param_grid=forecaster_param_grid)

model_selection.fit(y_train_preprocessing)

model_selection.best_forecaster_, model_selection.best_score_

(MultiplexForecaster(forecasters=[('VAR', VAR()),

('AutoETS',

AutoETS(auto=True, n_jobs=-1, sp=12))],

selected_forecaster='VAR'),

12.55874857841008)

# list hyperparameters of the select model

model_selected = VAR()

model_selected.get_params()

{'dates': None,

'freq': None,

'ic': None,

'maxlags': None,

'method': 'ols',

'missing': 'none',

'random_state': None,

'trend': 'c',

'verbose': False}

from sktime.forecasting.model_selection import ForecastingGridSearchCV, SlidingWindowSplitter

# create search list for each needed hyperparameter

param_grid = {'ic':['aic', 'fpe', 'hqic', 'bic', None], 'trend': ['c', 'ct', 'ctt', 'n']}

# create cross-validation approach

cv = SlidingWindowSplitter(window_length=10)

# grid search

gscv = ForecastingGridSearchCV(model_selected, strategy="refit", cv=cv, param_grid=param_grid)

fine_tuning = gscv.fit(y_train)

# get the best model

# the best model has been trained by the whole training data

model_best = fine_tuning.best_forecaster_

fine_tuning.best_params_

{'ic': None, 'trend': 'n'}

import numpy as np

# build pipeline

forecaster = (preprocessing * model_best)

fh = np.arange(1, 5)

forecaster.fit(y_train)

TransformedTargetForecaster(steps=[Detrender(forecaster=PolynomialTrendForecaster()),

FunctionTransformer(func=<function forward_transform at 0x1317374c0>,

inverse_func=<function backward_transform at 0x131737560>),

VAR(trend='n')])In a Jupyter environment, please rerun this cell to show the HTML representation or trust the notebook. TransformedTargetForecaster(steps=[Detrender(forecaster=PolynomialTrendForecaster()),

FunctionTransformer(func=<function forward_transform at 0x1317374c0>,

inverse_func=<function backward_transform at 0x131737560>),

VAR(trend='n')])from sktime.performance_metrics.forecasting import mean_absolute_percentage_error

# predict on test period

y_pred = forecaster.predict(fh)

# evaluation with metric

mean_absolute_percentage_error(y_test, y_pred, symmetric=False, multioutput = 'raw_values')

array([0.04696546, 0.0090055 , 0.10562995, 0.08357784, 0.00866678])

y_pred

| GNPDEFL | GNP | UNEMP | ARMED | POP | |

|---|---|---|---|---|---|

| Period | |||||

| 1959 | 109.820356 | 481987.985076 | 3521.913248 | 2708.821245 | 123198.414594 |

| 1960 | 110.185181 | 500509.160600 | 3688.966919 | 2839.922126 | 124772.422035 |

| 1961 | 109.431670 | 521129.199354 | 3701.676250 | 2797.859163 | 126323.296072 |

| 1962 | 108.267828 | 541203.882154 | 3787.301808 | 2670.374107 | 127921.498483 |